- Thinking about whether Ollie’s Bargain Outlet Holdings is actually a good deal right now? You’re not alone. Plenty of investors are looking for the real story behind the stock’s value.

- The share price has climbed by 24.4% over the past year and is up 13.7% year-to-date. However, it dipped slightly by 1.0% in the last week, which hints at dynamic sentiment and shifting expectations around its future growth.

- Recent headlines have highlighted Ollie’s retail expansion efforts and the company’s growing customer base, fueling optimism among investors. At the same time, broader retail sector trends are prompting some to wonder if the pace of growth can continue in this competitive landscape.

- On our valuation checks, Ollie’s scored 0 out of 6 for being currently undervalued. This is worth examining further as you weigh its prospects. We will break down how different valuation methods compare and offer a clearer perspective at the end of this analysis.

Ollie’s Bargain Outlet Holdings scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Ollie’s Bargain Outlet Holdings Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s dollars. This method provides a detailed perspective on what the business could be worth based on its ability to generate cash in the future.

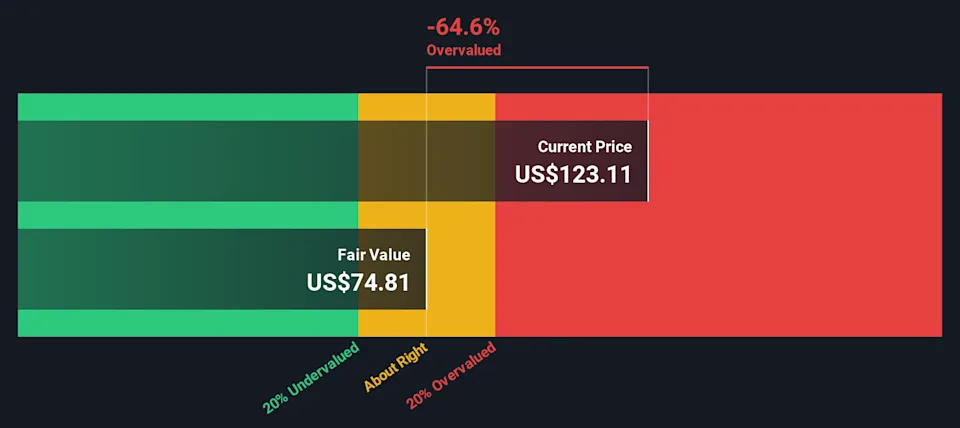

For Ollie’s Bargain Outlet Holdings, the DCF analysis starts with its recent Free Cash Flow of $131.9 million. Analysts have forecasted this number to steadily grow, with projections reaching $234.0 million by 2028. Looking even further ahead, longer-term estimates suggest Free Cash Flow could grow to roughly $348.6 million by 2035. While analyst projections cover the first few years, later figures are extrapolated using consistent growth trends to provide a longer-term outlook.

Based on these projections and calculated using a two-stage process, the DCF model estimates Ollie’s Bargain Outlet Holdings’ intrinsic value at $74.81 per share. Comparing this to the current trading price, the model indicates the stock is trading about 64.6% above its fair value, which suggests it is significantly overvalued according to this approach.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Ollie’s Bargain Outlet Holdings may be overvalued by 64.6%. Discover 914 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Ollie’s Bargain Outlet Holdings Price vs Earnings

The Price-to-Earnings (PE) ratio is one of the most widely used metrics for valuing profitable companies like Ollie’s Bargain Outlet Holdings. It is a straightforward way to see how much investors are willing to pay today for each dollar of the company’s earnings. This makes the PE ratio especially useful when the business is consistently profitable, providing a direct link between its share price and actual earnings.

What counts as a “normal” PE ratio can vary depending on a company’s growth prospects and perceived risks. Fast-growing or lower-risk businesses usually command higher PE ratios, while slower-growing or riskier firms tend to trade at lower multiples. For Ollie’s, the current PE ratio stands at 35.38x, which is noticeably higher than both the industry average of 19.96x and the peer average of 17.78x. At first glance, this could suggest the stock is trading at a premium relative to its sector.

Simply Wall St’s proprietary “Fair Ratio” offers a more tailored benchmark. It factors in expected growth, profit margins, risks, market cap, and industry context to arrive at a fair valuation specific to Ollie’s. This approach is more comprehensive than simple peer or industry comparisons because it accounts for unique factors shaping the company’s actual prospects and risk profile. For Ollie’s, the Fair Ratio is calculated at 18.88x, significantly below the company’s current multiple. This gap indicates that, even after adjusting for Ollie’s specific strengths and risks, the stock appears overvalued using this method.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1437 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Ollie’s Bargain Outlet Holdings Narrative

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple, powerful way to connect the story you believe about a company with its financial forecast and resulting fair value, making your investment view much more than just a number. On Simply Wall St’s Community page, used by millions of investors, Narratives help you put your assumptions about Ollie’s Bargain Outlet Holdings, such as estimates of future revenue, margins, and earnings, into a clear projection that can be updated instantly when new company news or earnings are announced.

With Narratives, you can easily see whether your story for Ollie’s supports buying, selling, or holding the stock, as each Narrative dynamically calculates a Fair Value based on your view and compares it to the current share price. Investors all see the same data, but Narratives let each person bring their own perspective. One investor might be bullish and estimate a fair value at $159 based on optimistic growth and margins, while another is more cautious, setting a lower fair value at $130. No matter your outlook, Narratives give you an accessible, always up-to-date framework for making smarter investing decisions rooted in both story and numbers.