Oil tumbled after US President Donald Trump said the Iran war will end soon, as he faces mounting pressure over the conflict that’s upended global energy markets and sparked concerns about an inflation crisis.

Brent and West Texas Intermediate both tumbled more than 10% before clawing back some losses, after a dramatic session on Monday that saw extreme price swings. Trump’s efforts to calm the market prompted crude futures to retreat on Tuesday — on top of resolving the war, he would waive oil-related sanctions and get the US Navy to escort tankers through the Strait of Hormuz.

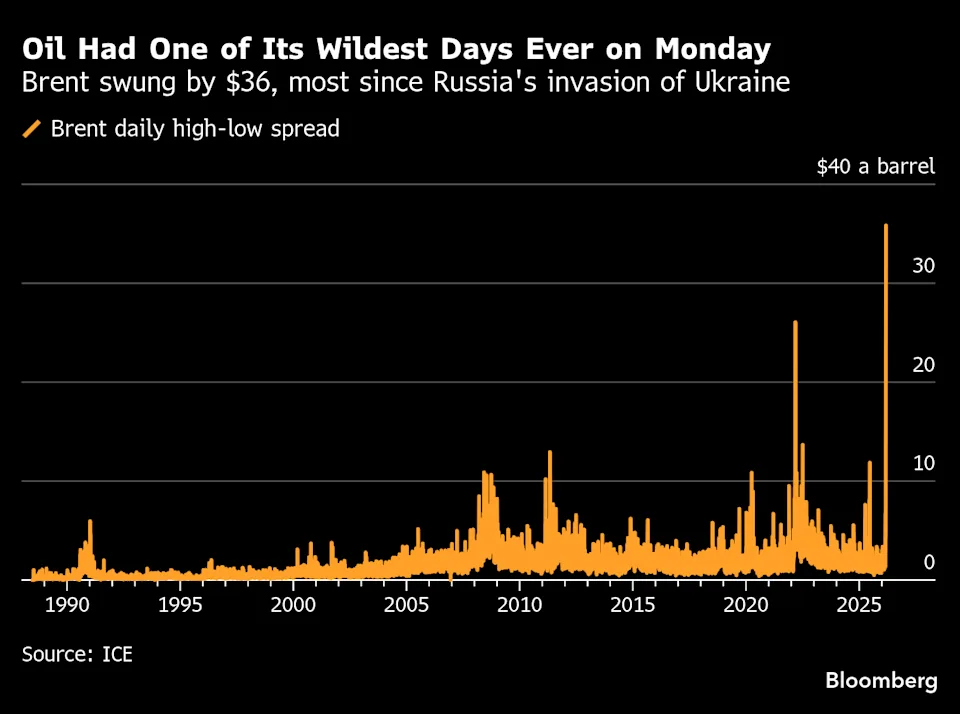

Global benchmark Brent was fluctuating around $93 a barrel after smashing through and holding above $100 for most of the previous session. The intense swings on Monday saw Brent trade in a band of about $36, the most on record and the widest range since Russia invaded Ukraine in 2022.

The conflict, which is now in its second week and has sucked more than a dozen countries into the fray, has led to a surge in energy prices, including oil, natural gas and products such as gasoil. US retail gasoline has jumped to the highest level since August 2024, putting additional pressure on Trump.

Oil soared toward $120 a barrel on Monday after major producers in the Persian Gulf were forced to cut output because of the effective closure of Hormuz — the narrow waterway that typically handles a fifth of global oil flows. Prices pulled back later in the session as the world’s largest economies considered an effort to release emergency reserves, and fell further on Trump’s war outlook.

Still, shipping through Hormuz is at a trickle, with the attack of multiple vessels since the war started on Feb. 28 leading most to shun the waterway. In recent days, a tanker hauling Saudi crude sailed across, while Iran has continued to ship large volumes, but trade is far from normal.

“Trump saying the Iran war will be over very soon is hardly the reassurance that will get tankers sailing normally again in and out of the Strait of Hormuz,” said Vandana Hari, founder of analysis firm Vanda Insights.

Investors have been skeptical about moves by the Trump administration to calm energy markets, but his latest remarks underscored a new willingness by the White House to publicly indicate that it could be moving to end the war.

The US president didn’t offer additional specifics on the plan to escort tankers or waive oil-related sanctions, beyond acknowledging he had discussed the topic with Russian President Vladimir Putin in a phone call earlier Monday. Last week, the Trump administration cleared the way for India to temporarily increase its purchases of Russian crude, reversing months of pressure on the trade.

“We’re looking to keep the oil prices down,” Trump said. “They went artificially up because of this excursion,” he said, adding that he did not believe the conflict would be over this week. At the same time, the US leader acknowledged unanswered questions that remained about the leadership in Tehran and vowed he would “not relent until the enemy is totally and decisively defeated.”

Saudi Arabia, Iraq, Kuwait and the United Arab Emirates have all reduced output as storage rapidly fills due to the Hormuz closure. The squeeze on crude and oil product flows from the Middle East has led to refiners halting some operations and deliveries, and Asian energy buyers outbidding rivals to lure fuel shipments that were originally headed to other regions.

The start of trading for WTI on Tuesday was temporarily stalled after a circuit-breaker halt in the first two minutes, further testing the limits of investors. On Monday, the US benchmark swung in a $38 band, the widest range since prices briefly turned negative during the depths of the pandemic. Futures are still more than $20 a barrel higher than pre-war levels.

“It’s unprecedented, even for as volatile as oil is,” said Vikas Dwivedi, an oil and gas strategist at Macquarie Group, who characterized trading on Monday as a “crazy day