Bonds sold off on Friday in a sign that investors expect the Federal Reserve to be more hawkish on interest rates amid concerns that surging oil prices could drive up inflation.

The 10-year Treasury (^TNX) yield, which moves inversely to bond prices, jumped as high as 4.46%, its highest level since July, as President Trump’s postponement of strikes on Iranian infrastructure failed to calm investor anxieties.

“After months of expecting the Federal Reserve Board to cut interest rates this year, investors have returned to a familiar refrain: ‘Higher for longer,'” wrote Mike Dickson, head of research and quantitative strategies at Horizon.

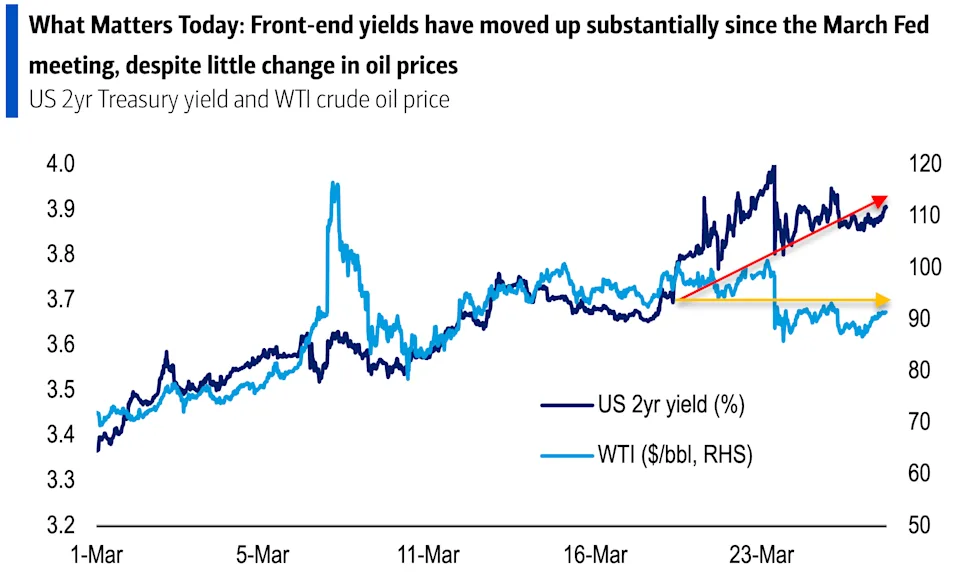

The 2-year Treasury yield’s climb to 4% on Friday suggests a similar scenario. The yield’s divergence from oil prices is notable, according to Bank of America US economist Aditya Bhave.

Over the past 10 days since the Fed’s meeting, futures on the US oil benchmark, West Texas Intermediate (WTI) crude (CL=F), have remained flat, down less than 1% over that period. Futures on international benchmark Brent (BZ=F) have lost roughly 3%.

Data from the CME shows investors now think the odds are roughly 20% the Fed will raise rates by its September meeting and assign no probability to a rate cut in six months. One month ago, the odds of at least one rate cut by September were greater than 90%.

Fed Chair Jerome Powell’s comments after the Fed’s meeting earlier this month were hawkish, and Fed governor Christopher Waller “sounded very concerned about the oil spike” in an interview on March 20, Bhave wrote in a client note Friday morning.

Given the post-meeting split between short-term rates and oil prices, “we think markets are now anticipating a more hawkish Fed reaction function and, possibly, a broader commodity shock,” Bhave wrote.

Bettors on Polymarket are pricing in a 40% chance that there will be no rate cut in 2026, and a 25% probability of a Fed rate hike later this year. (