There are people who haven’t checked their bank statements in months, and there are others who compulsively review their balances, transactions (pending and completed), and app alerts several times a day.

If you know where your money goes, and aren’t working toward any specific goals at the moment, operating on cruise control may be fine for a time. But if you have short-term plans (such as growing your savings or saving for a vacation) or longer-term aspirations (like saving up for a down payment, paying off a large amount of debt in a concise amount of time), tracking your expenses in a more dedicated way is key.

One popular way to do so is by using an Excel spreadsheet — something we often see among Money Diarists, like this Money Diarist and her husband, who live in Astoria, Queens and keep their expenses separate. “I keep track of charges on our credit cards on an Excel sheet and either attribute charges to him, myself, or as a split cost,” she explained.

By contrast, this Twin Cities couple joined forces and finances to pay off nearly $162,000 in debt in three years. They used a spreadsheet to keep them on target as they wiped out their debt.

If you haven’t created a spreadsheet like this before, you may be unsure how to set yourself up for Excel and money-saving success. So, we asked two young women who created spreadsheets for their budgets to share examples of how they tracked everything, and give a few tips.

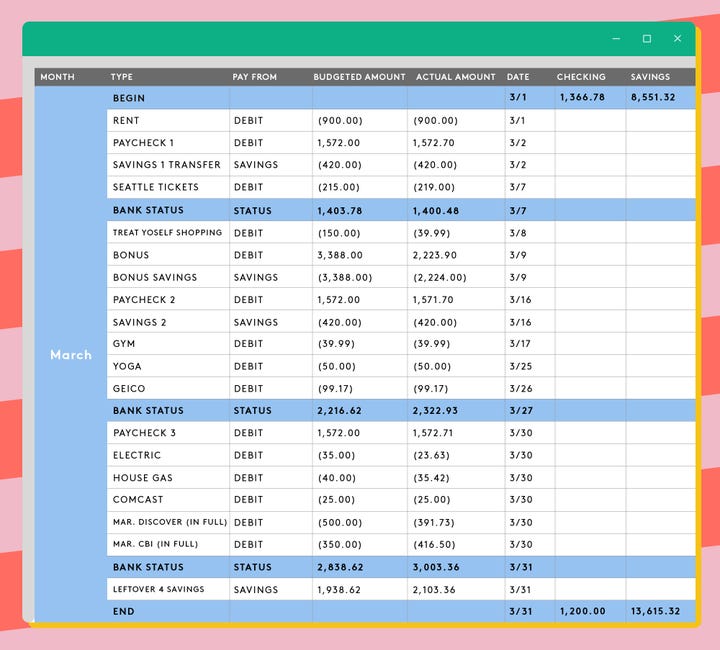

Option 1

Budgeter 1 says she developed her own system five months into her first real salaried job. As she wrote in her Money Diary, she “saved almost no money” when she first started working, and now checks her budget once or twice per week — with the goal of saving $10,000 by the end of 2018.

“I realized I was putting absolutely no money into savings and was spending frivolously. Now, I check in on the budget at least one or two times a week,” she tells Refinery29. “While that may seem like a lot, this Excel sheet helps me track where my money is going and has increased the amount of money I’m saving tenfold!”

She highlights rows in blue after the money has been paid off or transferred to give herself “a visual cue of [payments] that are still to come.” She also color codes items red or green depending on if the amount was higher or

lower than she budgeted.

Her biggest change has involved shifting her expenses from primarily debit to credit (something Stash Wealth founder Priya Malani evangelizes).

“I split my spending on two credit cards and then pay them in full at the end of the month,” Budgeter 1 explains.

“This system makes me more aware of what I’m spending and is slowly building my credit.”

Option 2

Budgeter 2 has a much more intricate approach.

“I update my spreadsheet a few times a week and use it in conjunction with Mint and my banking apps. I save this on Google Drive so I can access it wherever,” Budgeter 2 tells Refinery29. “At some point, this is probably unnecessary once you get the fundamentals down with budgeting. But I enjoy doing it, so I’ll stick with it for a while.”

She says tracking expenses in a spreadsheet helps keep her mindful of her spending and conscious of when she might need to “pull back” in certain categories if she has overspent in others. Color-coding also helps: She highlights sections in green where she is under budget in a given category, yellow if she’s on target, and red if she is over budget.

“It’s not a perfect system,” she said, “but it works for me.”

Her tips for making this system work in your own life:

1. Don’t obsess: If taking a consistent look at your spending is new to you, becoming better acquainted with your spending habits might be a little anxiety inducing at first. But the point isn’t to stress yourself out — and in fact, it’s the opposite. Things will get easier over time, so update it every few days without punishing yourself. Remain an honest but objective observer.

2. Make it fun: For some people, incorporating small games or challenges into tasks like these can be motivating. Budgeter 2 suggests trying to see how many zero-spend days you can achieve in a month, once you have a better understanding of your cash flow.

3. Audit yourself: After a certain amount of time, you’ll need to turn your observations into action. This might happen best once a larger cycle of time has passed, perhaps a season (about four months) or even half a year. (That way, you’ll have a more reliable understanding of your long-term spending habits, including splurges and special events. “Look back on old months to recognize trends in spending — e.g. how much money have I spent total on clothes this year? How did that feel? Could I have spent more/less?”

4. Be flexible: No one is perfect, and some weeks or months, you might decide to treat yourself. Don’t let a small splurge throw you off track. “I often go over budget in certain categories, but then I’ll try to dial back elsewhere in the next month,” Budgeter 2 says.

5. Do what works for you: Your spreadsheet might look different based on your needs. Use others’ methods as suggestions, rather than cleaving to a style that doesn’t work for you. “Edit this (or make your own) to customize, based on what you want to keep track of,” Budgeter 2 advises. “Not everyone wants to track daily spending like I do!”