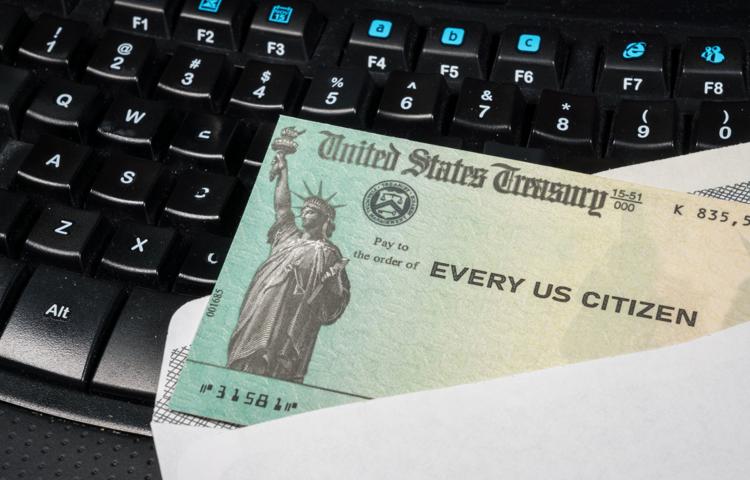

Millions of Americans will receive checks for up to $1,200 per person ($500 for each young child) as part of the $2 trillion stimulus package to ease the economic impact of the coronavirus pandemic.

Many families will need to use their checks to put food on the table or keep the roof over their heads. But if you’re working, consider putting your stimulus check to work.

“The beauty of the situation is there are no stores open, so it is much more difficult to waste your stimulus check,” said Andrew Marshall, a certified financial planner in Carlsbad, Calif. “Instead of buying something you really don’t need, put it toward a goal you have.”

Save for retirement: If you haven’t funded a Roth or traditional IRA for 2019, there’s still time to make a contribution that can lower your 2019 tax bill.

When the IRS extended the tax filing deadline to July 15, it also extended the deadline to contribute to a 2019 Roth or traditional IRA. The maximum contribution for a 2019 IRA is $6,000 — $7,000 if you’re 50 or older — so you can stash your entire stimulus check there if you don’t need it for anything else.

Pay off high interest rate debt: Interest rates have dropped on student loans, mortgages and bank savings accounts, but if you’re carrying credit card debt, you’re probably paying upwards of 15%. You can free up a lot of cash by paying off those cards.

Give it away: If your finances are in order and your job is secure, consider using your stimulus check to help those who don’t share your good fortune.

You can deduct a portion of your donations on your 2020 tax return even if — like most taxpayers — you claim the standard deduction. To encourage more charitable giving, the federal stimulus package includes a provision that allows taxpayers to claim a new “above-the-line” deduction for up to $300 in cash donations.

Shore up your emergency fund: Ideally, you should have at least three to six months’ worth of living expenses in a savings account. If you’re not there yet, your stimulus check is a good start.

Invest in a child’s education: Contributions to a 529 college savings plan grow tax-free, and withdrawals aren’t taxed if you use them for qualified expenses, such as college tuition and room and board. You can invest all or a portion of your stimulus check — 529 plans typically have low minimums. Plus, your state might give you a tax deduction or credit if you invest in your own state’s plan.