The economic shock from Covid-19 may call for drastic measures, but negative interest rates are not one of them — at least not yet.

The Federal Reserve has never brought its benchmark rate into negative territory and, according to Fed Chairman Jerome Powell, the central bank is not considering going to negative interest rates now.

Experts agree. “I view that as an eventuality but not in the near term,” said Greg McBride, chief financial analyst at Bankrate.com.

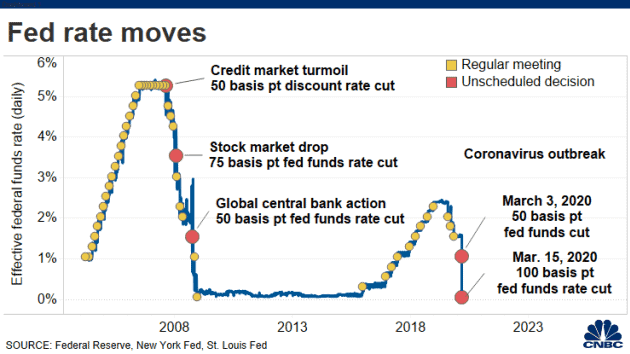

The Fed has already taken several aggressive steps to preserve the flow of credit, including slashing interest rates to near zero and pumping liquidity into strained areas of the financial markets. What comes next is the challenge.

President Donald Trump has been advocating for negative interest rates long before the coronavirus pandemic brought the economy to a standstill, arguing that erasing borrowing costs would spur economic growth.

“Negative interest rates sound like fun, but it’s nothing to wish for,” McBride said.

“It hasn’t even proven to be effective,” he added. “Parts of Europe have had negative interest rates for seven years and it hasn’t done anything — their economies were reeling then, they’re reeling now.”

And even if the federal funds rate, which is what banks charge one another for short-term borrowing, fell below zero, that is not the rate that consumers pay.

The prime rate, which is the rate that banks extend to their most creditworthy customers, is typically 3 percentage points higher than the federal funds rate.

For everyday Americans, negative interest rates would likely result in even lower mortgage rates and credit card rates, but “nobody is going to pay you to take out a loan,” McBride said.

In fact, with so many people under severe financial strain, its getting harder and harder to borrow at all.

Despite already rock-bottom interest rates, banks are tightening lending standards across the board, shrinking the availability of credit.

It’s more likely that savers will lose any benefit to stashing cash, said Tendayi Kapfidze, chief economist at LendingTree, an online loan marketplace.

“The detrimental effects to savers are immediate and clear,” he said. “This erodes earnings for savers and may force them into more risky financial instruments in search of yield.”